- Sixty percent of mines miss their own guidance, costing the industry $64 billion in five years.

- Mine productivity has dropped 25% since 2005, despite heavy investment in new technology.

- Author says miners keep buying quick fixes instead of fixing broken operations underneath.

SIXTY percent of the world’s mines report results at or below the lower half of their own production guidance, according to Accenture’s Billion Dollar Blind Spot report, a shortfall that has cost the industry $64 billion in lost forecast revenue over five years.

This isn’t analysts’ guidance, or a stretch target set by a nervous board. It’s the mine’s own guidance, built on the mine’s own data, set by the mine’s own leadership. You have better odds in a coin flip.

This study began analysing company reports before COVID-19, and the picture remains the same today. It isn’t a one-off. It’s a trend, and one nobody seems willing to talk about.

The pattern underneath the explanation

When we ask site teams why they missed guidance, the explanations are always specific: force majeure, key person risk, equipment failure, unrealistic plans. All of those things happen, but none of them is the whole truth. Most of them are also avoidable.

The whole truth is that the same shortfall shows up across different sites, different commodities, and different jurisdictions. See this pattern enough times, and you find the same structure underneath every one: the operation could not reliably deliver what it had promised. It relied too heavily on process workarounds, certain individuals, delaying maintenance or chasing higher grades at the cost of future faces.

According to the McKinsey MineLens Productivity Index, mine productivity is roughly 25% lower today than it was in 2005, even after controlling for grade decline and depth. Think of the billions the industry has spent on plant, technology, and people in that time, only for productivity to have fallen.

The bottom line? Miners are spending more to get the same amount out.

That is the Execution Gap, the structural distance between what leadership promises and what the operation can reliably deliver. A gap that is so consistent and long-running it has become structural.

What the industry keeps buying

There is a reflex that kicks in when a site misses guidance. Leadership reaches for something new, something you can name, approve, and announce. We call these Silver Bullets, and they fit into four categories: Technology, Asset, Methodology, Inspiration; TAMI, for short.

The Technology bullet: a new software platform, autonomous trucks, dashboards, and tablets. The investment is real. But the data feeding the tool is unreliable because the underlying process is broken.

Six months later its shelf-ware: an expensive programme gathering dust while the operation underneath carries on unchanged.

The Asset bullet: CAPEX approval for a bigger processing plant, new big yellow toys to move more material. On paper, nameplate capacity lifts 30%.

In practice, the same broken planning habits, the same reactive maintenance culture, the same undisciplined shift handovers migrate to the new plant. You have built a more expensive version of the same bottleneck.

The Methodology bullet: consultants arrive with Lean, Agile, or Six Sigma. Without fixing leadership, accountability, and culture underneath, waste is reduced, but the system is still broken. The consultants leave and so do the results.

The Inspiration bullet: leaders go to training, isolated from their day job. They come back energised. Nobody holds them to account.

A once-off, like a sheep-dip, with no ongoing inoculation.

Each one promises transformation. Each one adds complexity to an operation that was already struggling.

Add to that EY’s 2024 finding that 74% of mining and metals executives identify technology integration as a key challenge, against 37% across every other industry. Mining’s own executives are telling you they cannot absorb what they keep buying, at nearly double the rate of the rest of the economy.

The silver bullet is not the fix. It is a way of avoiding naming the real problem.

The real problem

The real problem is not the tool. It is what the tool has to land on.

Every site runs on what we call Operational Capability, which is the invisible engine that turns strategy, people, systems, culture, and leadership into repeatable results. It never makes the slide. It has no line in any budget or P&L, yet it is what determines whether any investment, any technology, any methodology actually delivers.

A site with strong operational capability absorbs a new system and pulls value from it. A site without it watches the same system sit idle within six months.

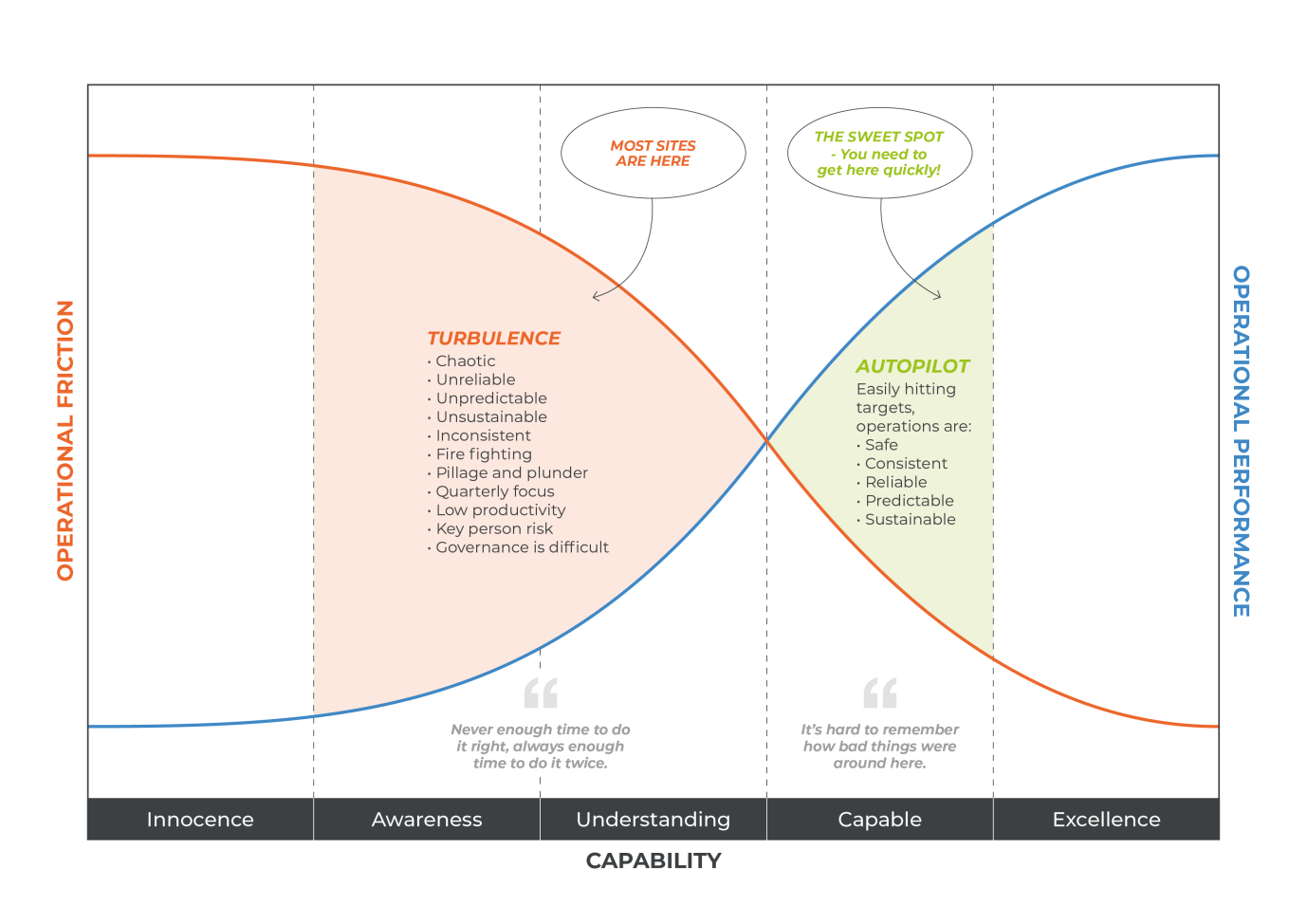

We map this operational maturity on the capability curve, from Innocence at one end to Excellence at the other. Most sites sit somewhere in the Turbulence Zone: reactive, heroics, and constant firefighting. Just look at the variability between the best and worst day’s production, when everything goes right, or wrong.

Sites here are already running at their capability capacity. Adding complexity in the form of silver bullets and you get the same result, faster.

The rare few sites that sit in what we call the “Autopilot Zone” are a different world. Results are predictable. Chaos has been engineered out, not muscled through.

The GM is no longer the circuit breaker for every production variance. That is the state that can take a new tool and turn it into a durable advantage.

The difference between those two worlds is not geology or commodity price. It is capability. These are the sites working smarter, not just harder.

History already ran this experiment

This is not a new problem. The result is in the economics textbooks.

In the 1890s, U.S. textile mills replaced their steam engines with electric motors. The technology was plainly superior. For 30 years, almost nothing changed; output barely moved.

The mills had swapped the motor but left the factory untouched — same floor plan, same line shafts, same jobs, economist Paul A. David wrote in his 1990 paper “The Dynamo and the Computer” published in the “American Economic Review.”

The gains arrived when a generation of factory owners stopped retrofitting and rebuilt from scratch. Equipment arranged by the flow of work. Different roles for the people on the floor.

Once that rebuilding happened, electrification drove roughly half of all U.S. manufacturing productivity growth through the 1920s. The return was never in the technology, it was in the application.

Mining is in the middle of the same lag. We are applying technology as the solution, not as part of a bigger operation.

The steel industry ran the same experiment. Bethlehem Steel was the tier-1 incumbent. When the electric arc furnace arrived, Bethlehem could have bought one.

What it could not do was change how it operated. Nucor, a case study in the book “Good to Great,” rebuilt around this new furnace technology, like the mills did. It went from near-bankrupt to the most profitable steel producer in America.

Bethlehem filed for bankruptcy in 2001. The furnace was the multiplier. The operational capability was the engine.

Add AI, automation, or robotics to a mine still run the old way, and you get Bethlehem with better tools.

The choice at the crossroads

For tier two and three operator with larger capital constraints, the crossroads looks like this:

Option one: reach for the silver bullet. Buy the platform. Commission the expansion.

Bring in the consultants. Arrive at the same crossroads next year.

Option two: name the real problem. Diagnose capability honestly: the kind that finds root causes, not the kind that confirms what the board want to hear. Build the planning discipline before buying the planning software.

Fix the shift handover before automating it. Build the operation that can leverage the tool rather than buying a tool to fix operational performance.

The sequence matters. McKinsey found that roughly 70% of digital pilots in mining capture no meaningful value.

The pilots do not die on bad technology. They die because the operation underneath was not ready.

Technology deployed onto a capable operation compounds. Technology deployed onto a broken one scales the chaos, faster and at greater cost.

The miners that close the Execution Gap do not have better technology. They have better operations, and the discipline to build them before the next investment cycle.

That is Operational Alpha: the durable advantage that accumulates when capability compounds. In a commodity cycle, where price and geology are given, it is the only remaining alpha. And, unlike a technology platform, it cannot be purchased by a competitor.

The crossroad is real. The direction is a choice.

The question for any GM reading this, sitting between the board’s ambition and the site’s reality, is not which silver bullet to reach for next. It is whether you are willing to name the thing you have been avoiding, and start building the operation that can actually deliver.